Belief is absent and hard to restore

If the government was hoping that last month’s agreement with the institutions at the Eurogroup in Luxembourg would mark a sea change in the way that Greeks view their economic future, the opinion polls published since the June 15 meeting will have delivered a sobering reality check.

The surveys show that Greeks are not convinced that the deal struck to provide Greece with another 8.5 billion euros in bailout funding and to move the debt sustainability discussion on a little further will make a marked difference to their lives. Also, according to the polls, they are not convinced that their country is now on a path that will lead it out of the crisis.

A University of Macedonia poll for Skai TV made public last Monday indicated that only 10 percent of Greeks believe the country is on the way out of the crisis as a result of the Eurogroup agreement, whereas 82.5 percent believe that Greece was condemned to constant austerity at the meeting in Luxembourg.

The pollsters also found that only 7 percent of Greeks believe that their financial situation will improve in the next 12 months.

Of course, this is partly related to the government’s failed strategy. Just 16.5 percent think it negotiated effectively on the debt issue, according to the poll conducted for Skai, and only 13 percent of Greeks believe the government got what it wanted from the Eurogroup agreement.

However, other polls also suggest that the negative sentiment goes beyond the misadventures of the SYRIZA-Independent Greeks coalition and that it reflects a broader fatigue that has undoubtedly been exacerbated by the events of the last couple of years.

A Kapa Research poll published in previous Sunday’s To Vima indicated that only 23.5 percent of respondents believe that Greece and its economy are close to the point of leaving the difficult years of the crisis behind, while 76 percent think that this is not the case.

A recent poll by ProRata for Efimerida ton Syntakton daily showed that 19 percent of those questioned agreed to a lesser or greater extent that the Eurogroup agreement reached on June 15 opens the path for Greece to exit the bailout and the crisis. An overwhelming 75 percent did not agree that this is the case.

According to the survey, Greeks’ most prominent feeling about the agreement was disappointment (35 percent), followed by indifference (16 percent) and stress (15 percent). Just 5 percent said the deal filled them with optimism or enthusiasm.

Apart from the weariness caused by the interminable crisis and the government’s slipups, this negativity may also be caused by the numerous loose ends that the June 15 agreement leaves. When the national mood is pessimistic, any uncertainty is likely to be transformed into a worst-case scenario in many people’s minds.

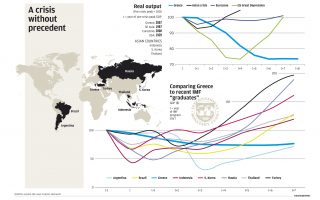

One issue that the agreement did not resolve is debt sustainability. The extent to which this is still a source of great uncertainty was underlined in the debt sustainability analysis (DSA) put together by the European Commission and published along with the Compliance Report issued by the institutions.

The DSA deals with four scenarios going forward. Scenario D assumes an average nominal GDP growth of 3.5 percent between 2019 and 2060, the primary surplus is seen at 2.3 percent in the period between 2023 and 2060, while the debt-to-GDP ratio is expected to plummet to 75.4 percent by 2060. This is the best-case scenario.

In the worst-case scenario, C, there will be average nominal GDP growth of 2.7 percent between 2019 and 2060, while the primary surplus is seen at 1.5 percent of GDP from 2023 onward. The debt ratio is expected to fall to 141.1 percent in 2030 and start rising to 185.8 percent in 2050 and 241.4 percent in 2060. Clearly, this would be a disastrous outcome for Greece as it would end up with a much higher debt ratio than the one of around 180 percent it has now.

Scenarios A and B are somewhere between the two, leaving debt ratios of 91.7 percent and 139 percent respectively. Clearly, there is ample room for doubt given the yawning gaps between the various scenarios, particularly the two at either end of the spectrum.

The formula for addressing this is well-known and set out clearly in the Compliance Report. It consists of “sustained implementation of the far-reaching reform program” (including “strong ownership on the part of the Greek authorities”) and “an appropriate combination of debt management measures.”

However, the DSA adds another element of doubt to the equation by pointing out that even if the two factors mentioned above are combined in the decades ahead, there are still other obstacles that could prevent Greece from ending up where it and its lenders would like.

“Debt sustainability, and thus the need for additional debt measures, should be assessed in a manner that caters for a number of downside risks,” it reads. “There is uncertainty surrounding the capacity of the Greek government to sustain high primary surpluses over several decades. In addition, there are significant downside risks to growth linked to aging populations and trends in total factor productivity.”

It is worth noting that the International Monetary Fund’s mission chief for Greece Delia Velculescu also mentioned the aging population as a cautionary factor for long-term targets during her contribution to The Economist Roundtable in Athens last week.

Given that Greece’s lenders are sharing publicly their hesitancy about the future, it is only natural that Greeks are unable to view the coming years with great confidence.

The question that should trouble Greece’s politicians is what could change this. Will a convincing agreement on debt relief (if such a thing is on offer) suffice to open the floodgates and bring confidence rushing back in? Will the return of growth and job creation trigger a change in mood or can the transformation be so gradual that many doubters will remain? Can the implementation of key reforms alter daily life and the way the economy functions to such an extent that the public mood is lifted? Can a change of government bring with it a wind of optimism that will sweep people with it? Are all of these things combined needed or will something else be necessary?

The only certainty when looking at the numbers as they stand is that something substantial is required to get Greeks believing again.