Update on the quarterly national accounts – Part 4

In this fourth Note on the quarterly national accounts, we mine for more data to see how the economy is evolving, and observe whether this provides information that we need to be aware of when thinking about government policy. Specifically, we will be trying to find out what aggregate demand components are providing the biggest push to growth in real GDP. This analysis of “contributions to growth in real GDP” can be helpful to see if the economy is growing in a sustainable or unsustainable way. It can also provide important clues about competitiveness.

What is the difference between a growth rate and a contribution to growth, you may ask? Let us assume that real GDP grows from 100 to 105 between two certain time points. We then would say that the economy has grown by 5 percent over this interval. We can further ask what are the contributions from domestic demand and net foreign demand, to see if this growth in the economy is well balanced or very much dependent on one source of demand or the other.

So, let us say, for the sake of argument only, that at the outset, domestic demand was 90 percent of real GDP and net foreign demand was 10 percent of GDP. Thus, real GDP starts off at 100 with domestic demand at 90 and net foreign demand at 10. Then in Period 1, domestic demand increases to 93 and foreign demand increases to 12, together making up the new real GDP of 105 mentioned above.

The rate of growth in domestic demand is then (93-90)/90 = 3.3 percent, and the rate of growth of net foreign demand is then (12-10)/10 = 20.0 percent. If we want to go back from growth rates in the components to the growth rate of the total (real GDP), we cannot add up the two growth rates and say that real GDP has grown by 3.3 + 20 = 23.3 percent. The reason for this is that domestic demand makes up so much bigger a share of total real GDP than net foreign demand – it has a bigger weight in determining overall real GDP growth.

To analyze how much each component contributes to overall growth we need to take the increment in each component, and divide this by GDP at the beginning period, to see how much each demand component advances the overall real GDP. This is a calculation that looks at the growth rate of each component weighted by its overall participation in real GDP in the beginning period. Thus, the contribution to growth of consumption is (93-90)/100 = 3 percentage points of GDP; and the contribution of net foreign demand is (12-10)/100 = 2 percentage points of GDP. Now the two contributions add up to 5 percent overall growth. Three percentage points of 5 came from domestic demand and 2 percentage points of 5 came from net foreign demand.

Why should we care about this? In politics, it is sometimes interpreted that domestic demand is more important in generating growth than foreign demand, because of its bigger weight in the total, and thus “the government needs to stimulate domestic demand and pay less attention to the foreign sector.” When that becomes the view, it is likely that policy is designed to stimulate domestic demand, in turn dominated by consumption. Indeed, domestic producers may lobby the government and public opinion that if the government does not favor its domestic industry over the external traders, then the government is not representing well the majority of the public and of the producers in the country.

But this can end up making growth very unbalanced and much too dependent on domestic demand. If domestic demand is booming because of policy populism and net foreign demand is a policy orphan, the external deficit is likely to deteriorate, requiring the placement of external debt to keep this going. You get my drift – this is how countries get into unsustainable debts.

In some countries, the opposite effect can happen. Consider that in today’s conjuncture, Germany and the Netherlands are sometimes said to be favoring the external sectors as the engine of growth (with big surpluses), and that domestic demand is insufficiently developed or stimulated. Indeed, there are technical considerations for worrying about constant external surpluses too. But analyzing the cause of imbalances is no minor issue and countries can go through long cycles of growth led by one side or the other. There is moreover an unpleasant reality check: Running a deficit or a surplus is a bit like being in the swimming pool. If you run constant deficits, you may be said to be under water. If you run constant surpluses, you may be said to be above water. Who can hold out the longest? The real issue is not so much whether a country runs deficits or surpluses for a while (this can happen quite naturally for various reasons, without government intervention), but rather whether policy deliberately causes this effect either through neglect of external competitiveness (perhaps leading to deficits) or from a policy interference to keep the external sector strong (deliberately wanting surpluses). Since one country’s deficit must be another country’s surplus, this complex area of policy interaction gets us to the material of the global imbalances, which continues to be a delicate and indeed difficult policy question in international economic diplomacy.

Rather than pretending that we can do justice to such a complex global problem here, let us think about what data tell us for Greece and its contributions to growth of the various demand components. I am willing to make the statement that Greece should aim for a while at strengthening its external position and thus favoring a moderation of domestic demand, certainly consumption, and a strengthening of net external demand. The reason for my view is that stronger external performance will generate growth that is sustainable for a long period of time and that is needed to help control the debt. Economists sometimes refer to this as rotation in the sources of growth or as “moderating domestic absorption in favor of stronger external performance.” Improving efficiency and productivity will make the economy more competitive and thus favor a rebalancing to stronger external performance – the structure of aggregate demand will change and make Greece a more open economy with better prospects for growth sustainability and lower debt. We already saw in earlier notes that Greece is curiously more closed than the much bigger eurozone as a whole, and that domestic consumption is out of proportion, which is telling.

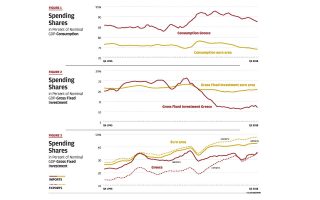

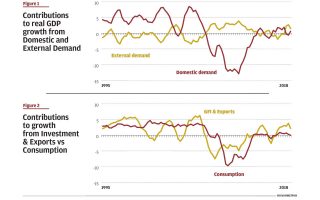

What happens if government policy ignores the structure of demand and contributions to growth? In the absence of reforms to favor efficiency and productivity, in some way, Mother Nature will then be doing this rebalancing the hard way through a deep recession, by lowering income and thus depressing domestic demand, and by lowering prices in Greece relative to trading partners to improve price competitiveness. This is the dreaded “adjustment through poverty scenario” that has been playing out in Greece. Thus, when the recession came, did we automatically see that the contribution to growth from the net foreign balance became greater than the contribution to growth from domestic demand? See Figure 1.

Here we see that Greece used to run large positive contributions to growth from domestic demand. That is to say, growth was strongly led by domestic demand and the contribution from the foreign balance was mostly negative – running worsening external deficits. This changed in the crisis when domestic demand collapsed and the foreign sector took over to lead growth with respectable contributions of around 2 percentage points a year. The numbers on contributions are additive, so the very large decline in domestic demand overwhelmed the good developments in the foreign balance during the depth of the crisis. Since 2015, domestic and external demand contributions have been roughly in balance. In 2018, the contribution from external demand was strong again, with more or less neutral contribution from domestic demand.

Thus, this development suggests that Greece has made good progress in strengthening the contribution from the external sectors since the crisis began, but this came at a high price of sharply lower domestic demand and income – the improvements came mainly through slower domestic demand, rather than boosting supply and efficiency in the economy. If policies could have focused more effectively on supporting efficiency gains and better competitiveness, which requires structural reforms in many areas, then Greece would have experienced a recovery in foreign performance without the need for as large a domestic contraction as has been experienced. This is the key reason why so many analysts encourage further structural reforms – policy would then work with the grain of Mother Nature and not against it. If you want to resist Mother Nature in rebalancing the economy, you are going to lose, so the art of good policy making lies in part in finding what Nature wants to do to rebalance. Then Greece not only gets higher, but also more sustainable growth.

Since there is a priority on the recovery of productive capacity and exports, I have plotted the contributions from gross fixed investments and exports (combined) below, against the contribution from consumption. This picture is also interesting. Figure 2 shows that the decline in the contribution to growth from fixed investments and exports preceded the decline in consumption. This may be related to consumption smoothing, which causes consumption to respond with a lag. Also, the recovery in investment and exports was interrupted in 2015 and 2016, but, fortunately, the economy has regained ground again with the recent stabilization.

Interestingly, consumption is now moderately behaved with no systematic contribution to growth since 2014. While this is structurally sound, it may be politically sensitive, because the public “feels” as if consumption is stuck, and it is less or not aware that things are going better with fixed investment and exports, which show a contribution of growth around 2-3 percentage points, which is quite good. So, I see merit in pointing out that there is good news in this Figure, because Greece needs strength in investment and exports more than it needs strength in consumption, from a sustainable growth point of view. It shows how important it is that the public receives good information so that it can see that not all the news is bad (slower consumption gains) and that the economy is actually showing tentative signs of turning around for the better. The ability to enjoy consumption will gradually follow the recovery in productive and competitive investments. It does not seem appropriate from where Greece is today that consumption is again pushed to lead the recovery.

We can follow these figures over time as new quarterly accounts become available to see if the promising indicators hold their strength in the medium term. It will be especially interesting to see if changes in government policy have an impact on the structure of demand and the various contributions to growth. One thing seems certain: Greece came from a long history of sharp imbalances in the economy (too much domestic demand – consumption) and not enough attention to productivity and efficiency in the economy. Turning around such an unbalanced structure and its legacy effects takes a lot of time – easily decades. Thus, patience and perseverance are important to continue to make progress. This loops back to saying that Odysseus, in his long-run plan in Note 13, is a patient man – he is willing to look forward to 2080 with a consistent policy approach before Greece recovers a 60 percent of GDP debt ratio and below.

Bob Traa is an independent economist. This is the 18th in a series of articles by him for Kathimerini titled “Notes for Discussion – Essays on the Greek Macroeconomy.”