Little hope six months after bailouts

It is just a few days over six months since Greece concluded its exit from the despised memorandums and the economic situation remains essentially unchanged. There is no light at the end of the tunnel. Instead there is another narrow tunnel, with continued budgetary surpluses, heavy taxation that takes the life out of private initiative, and a banking system weighed down by massive amounts of nonperforming loans, resulting in small income gains and continued massive unemployment.

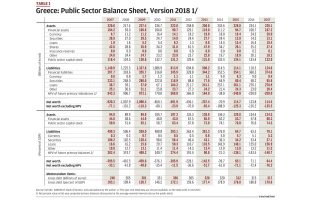

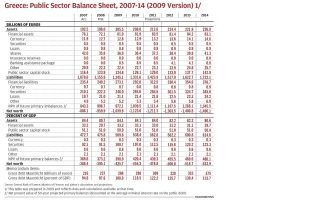

The recent European Commission report was depressing in two ways. First, because it gave a detailed account of the government’s weakening commitment to reform: While 13 of the 16 end-of-2018 specific commitments were met, the main achievement was the 3.5 percent budgetary surplus – the straitjacket that has been forced on Greece by its creditors so that it can continue to maintain service on its external debt. The surplus was in part achieved through the accumulation of new government arrears, contrary to the commitment the government made on this issue. And there were the usual increases in government employment, delays in privatization – what’s new? – as well as delays in the passage of new legislation to replace the so-called Katseli law protecting primary residences from foreclosure.

The second and main source of bad news is that there is no glimmer of hope that things will get better any time soon. There is no sector of the economy likely to provide a spark, a springboard for the rest. Investment, the usual engine of growth, continues to languish. Private investment is not growing because the banking system remains in the doldrums and little money is being given out in new loans. Public sector investment is just not happening: The latest numbers show that public sector investment in January 2019 was only two-thirds what it was supposed to be.

The bottom line is that growth in 2019 is likely to be at most an anemic 2.2 percent – slightly higher than the 1.9 percent achieved in 2018 – and will average about 2 percent for the next four years. The prospects for the tourism sector – the main engine of growth in 2018 – are worrisome. People do not expect it to replicate the very large growth achieved last year. Hotel occupancy rates in Athens are declining, as are prospective revenues. Exports, which rose 15.7 percent in 2018 (10.7 percent excluding oil), may be hurt by the slowing of the global and especially of the European Union economy. The only positive is that the recent increase in the minimum wage will put some money in the hands of people that really need it, resulting in a stimulus to what economists call consumption.

The Commission politely says, “Overall, the balance of risks is tilted to the downside,” meaning things are more likely to be worse than projected than better. One of the risks that nobody can control is what happens to pending decisions by the judiciary which could overturn previous pension reductions. If that were to happen, the costs could amount to 2 percent of GDP – that is, all the budget forecasts could be blown, which will cause the Commission and the rest of the institutions a serious headache and probably result in even more intrusive and detailed conditionality.

And what about the longer term? The Commission thinks the financial prospects are positive. The government floated a five- and a 10-year bond, each of 2.5 billion euros at slightly lower interest rates than expected. But the Eurogroup refused to release the 970 million euros held by the ECB of profits made on Greek bonds because the government failed to meet important end-of-year commitments, such as the law on foreclosures. The government hopes they will get the money in April.

The problem with all this is that it does not really matter unless it results in a new deal on the Greek debt which permits the Greek government to get out of the commitment to maintain a budget surplus of 3.5 percent for years. That surplus is a drag on the economy and the private sector. It will not permit a resurgence of growth that will curb unemployment and reduce the flow of Greek human capital abroad. The Commission forecasts that Greek unemployment in 2022 will be a socially unacceptable 14.4 percent, with youth unemployment probably more than double that figure. Add to that the burden of coping with refugees numbering 90,000 at the end of the year and one must agree with the Commission that the downside risks are high.

I called for such a new deal last year (see Kathimerini, August 5, 2018), but developments in Europe suggest that it is not likely to happen any time soon. There is a ray of hope in the agreement German Chancellor Angela Merkel and French President Emmanuel Macron announced recently for a eurozone budget which will be presented to the member-states. Yet, it is too much to expect that this budget will offer significant relief to Greece’s long-term problem of servicing its huge debt. There is the pressing matter of Brexit and its impact on European economies, the trade war threatened by US President Donald Trump, and the unpleasant ascendance of extremist parties everywhere. There is, finally, an uneasy feeling among many that the German and French visions of Europe are quite different. In all this turmoil, the problem of long-term Greek growth is bound to be viewed with benign neglect.

Greeks must get accustomed to puny growth of maybe up to 2 percent per annum, if that much, for many years to come – not that different from most countries in the eurozone. And we must do the best we can to straighten out the many inequities and inefficiencies in our society, including the sclerotic judicial system and chaotic university education. The saddest thing is that many have come to believe that we cannot do this on our own and need the detailed tutelage, prodding and conditionality of the technocrats of the Commission and the other institutions.

Constantine Michalopoulos is visiting scholar at Johns Hopkins University’s School of Advanced International Studies. He is former director of Economic Policy and Coordination at the World Bank and chief economist at the United States Agency for International Development (USAID).