Stress testing the financial sector’s resilience to climate change

Climate change has the potential to cause substantial disruption to our economies, businesses and livelihoods in the coming decades. Yet the associated risks remain poorly understood, as climate shocks differ from the financial shocks observed during previous crises.

Climate change occurs slowly over long periods, which creates significant uncertainty about how extreme climate events will materialise in the future. Both public and private institutions have a great deal of work ahead of them to effectively identify and assess the potential impact of these risks given that the traditional risk management tools may not suffice. With this in mind, the ECB has designed the first economy-wide climate stress test to help both authorities and financial institutions assess the impact of climate risks on companies and banks over the next 30 years.

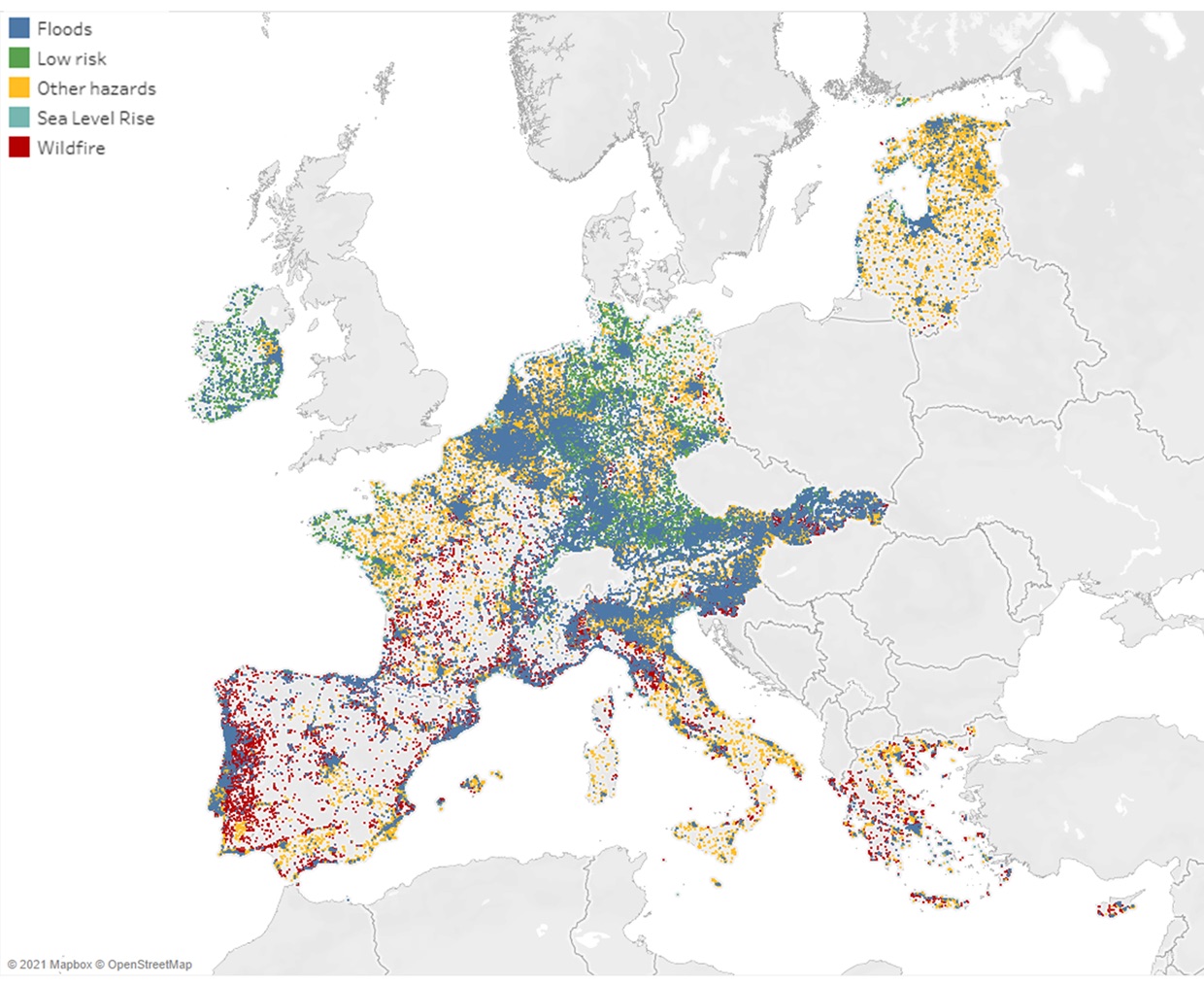

Typically, climate change risks are split into two broad categories. The first is physical risk, which stems from the expected increase in the frequency and magnitude of disasters caused by natural hazards. Businesses located in exposed areas, for example close to rivers or the seashore and therefore prone to flooding, could suffer significant damage should a climate event occur. This damage could interrupt the production process in the short term and potentially lead to business failure in the longer term. Physical risks differ across countries and regions, with southern Europe on average more susceptible to heat stress and wildfires, while central and northern Europe are more vulnerable to flooding.

Chart 2 A

Mapping of transition and physical risk for euro area firms

Source: ECB calculations based on the Four Twenty Seven dataset. Each dot corresponds to a firm in the sample. Gaps in the mapping are due to (a) economic activities being concentrated in specific industrial areas in some countries, and (b) Four Twenty Seven data not being available for latitudes above 60 degrees for flood risk. Other hazards include water stress, heat stress and hurricanes and typhoons. For simplicity only euro area firms are displayed in the chart, although data are available for a much broader sample.

The second category is transition risk, where the delayed or abrupt introduction of climate policies to reduce CO2 emissions could have a negative impact on certain energy and carbon-intensive industries, such as mining, cement or steel. Higher tax rates on carbon usage could, for example, increase production costs and reduce profitability.

Both physical and transition risks can harm financial stability if banks or other financial institutions are exposed to defaulting firms through their lending or asset holdings. Yet while it is common to distinguish between the two types of risk, in truth they are intertwined. Greater climate policy action may increase the impact of transition risks in the near term while simultaneously reducing the incidence of physical risks in future decades. The ECB climate stress test captures and quantifies this potential trade-off using a 30-year timeline to take account of the long-run impact.

The ECB climate stress test examines the resilience of companies and banks to a range of climate scenarios. These scenarios set out plausible representations of future climatic conditions while also accounting for the impact on businesses of measures taken to limit the extent of climate change, such as carbon taxes. The ECB scenarios are based on those provided by the Network for Greening the Financial System but have been adjusted to capture the relationship between transition risk and physical risk more thoroughly.

The orderly scenario considers the timely and effective implementation of climate policies which successfully limit global warming. The hot house world scenario considers the impact if no new climate policies are implemented and is associated with a very significant increase of physical risk in the medium to long run. The disorderly scenario considers the impact of a delayed and abrupt implementation of climate policies.

These scenarios, together with a unique dataset that identifies and quantifies transition and physical risk exposures for millions of companies worldwide, provide the background for analysing the impact of climate change on businesses and banks.

Preliminary results show that, in the absence of further climate policies, the costs to companies arising from extreme events increase substantially. The results also show that there are clear benefits in taking action early: the short-term costs of adapting to green policies are significantly lower than the potentially much higher costs arising from natural disasters in the medium to long term. Climate change thus represents a major source of systemic risk, particularly for banks with portfolios concentrated in certain economic sectors and geographical areas.

These results underline the crucial and urgent need to transition to a greener economy, not only to ensure that the targets of the Paris Agreement are met, but also to limit the long-run disruption to our economies, businesses and livelihoods.

* Luis de Guindos, Vice-President of the ECB. This article appeared as an opinion piece in the following publications: De Tijd (Belgium), Stockwatch.com.cy (Cyprus), Kauppalehti (Finland), L’Agefi (France), Börsen-Zeitung (Germany), Kathimerini (Greece), Il Sole 24 Ore (Italy), El Economista (Spain).