Agreement brings Greece closer to goal

The end of the soccer season is approaching and it is the time of year when coaches are assessed. This is when results, rather than performances, are what counts for fans and club owners. The same goes for political leaders, no matter how much Prime Minister Alexis Tsipras might try to argue differently.

Throughout his premiership, Tsipras has made a habit of putting emphasis on effort and intentions rather than the outcome. For instance, he has often spoken about the 17 hours he spent negotiating with eurozone leaders in July 2015, when Greece’s position in the single currency was on the line, but tends to skirt around the mistakes that put him in that position or the cost of the whole process.

So, having concluded a technical agreement with Greece’s lenders last week, it was no surprise that the SYRIZA leader talked up his government’s battling spirit and avoided dwelling on whether the result could have been better.

Tsipras admitted that his government did not want to cut pensions or lower the tax-free threshold but argued that it had averted some of the lenders’ more “irrational” demands to arrive at a “balanced and sustainable” agreement. The ultimate judgment, though, will come when voters are able to express their opinion on the deal. They will need more time to digest the implications but Tsipras can be sure that when crunch time comes, the result will count and not whether his administration had meant well.

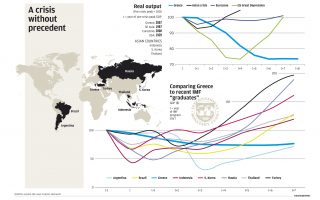

There are three key elements that will decide whether the agreement is seen as a success or not. The first will be how Greeks react to the new fiscal measures due to be passed through Parliament in the coming days. Then, there is the question of whether the expansionary countermeasures will be implemented and to what extent they will have an impact. Finally, the most important aspect is whether the deal reached in the early hours of last Tuesday provides a launch pad for the economy, allowing it to blast a path for Greece to exit the crisis.

In terms of the new fiscal measures – which consist of a 1 percent of gross domestic product reduction in pension spending and an equivalent revenue increase from the lowering of the tax-free threshold – the likelihood is that the SYRIZA-Independent Greeks government is in for a rough time.

It appears that many of those who will be affected by these measures have not yet realized their impact. The reduction in pension spending, due in 2019, means that retirees will see their income slashed by up to 18 percent, although the weighted average will be around 9 percent. Greek pensioners may have become used to seeing their earnings dwindle over the last few years (one retirees’ association calculated last week that there have been 23 reductions since 2010), but the cuts that are coming up are particularly deep even within the context of the Greek crisis. They will also affect a large amount of people since both main and auxiliary pensions will be affected. Kathimerini has estimated that some 1.1 million pensioners will be worse off.

Similarly, the reduction in the tax-free threshold for personal incomes, due in 2020, is dramatic and will also affect large parts of the population. It currently ranges between 8,836 euros for a single person and 9,545 euros for a family with three children. In three years, these figures will drop to 5,681 and 6,590 respectively, resulting in a significantly bigger tax bill for anyone earning more than these low amounts each year.

Tsipras and his ministers have tried to argue over the past few days that although these are painful measures, they will create the necessary fiscal space for the government to implement the expansionary interventions it has agreed with the creditors (on the condition that fiscal targets are met).

The countermeasures include some positive moves, such as a reduction in corporate tax from 29 percent to 26 percent, a lowering of the solidarity levy rates and cutting the lowest rate of personal income tax from 22 to 20 percent. The problem the government has is that even if it gets to adopt these measures, their individual impact will be relatively small. For instance, bringing down the initial income tax rate to 20 percent is worth 0.5 percent of GDP, while a lower corporate tax rate will account for just 0.2 percent of GDP, which is the same as the impact from bringing down the solidarity levy.

The coalition may also encounter this problem with its other countermeasures, which focus on increases to social spending. For example, extra housing benefits for vulnerable families may make a difference to those affected but represent an adjustment of just 0.2 percent of GDP, while only 0.1 percent of GDP will be spent on providing school meals in areas with high unemployment. This does not mean they are not worthwhile endeavors, but the government should not expect these initiatives to move the needle in political and economic terms.

The real testing ground will be whether last week’s agreement proves to be the moment that Greece drew a line under the “memorandum era” and moved on. This will depend on several factors. Firstly, the deal will have to provide Greece with the economic and political stability it needs to heal its wounds. Ideally, apart from triggering the release this summer of more than 7 billion euros of funding, much of which should be destined for paying off state arrears, the agreement should also convince investors that Greece now has some clear space ahead of it, stretching beyond the next couple of years.

For this to come together, though, Greece must have a degree of confidence that it will exit the program successfully next year. This will require an imminent agreement on debt relief that will be enough for Greek bonds to be considered eligible for the European Central Bank’s quantitive easing (QE) program. If this is the case, Athens can begin plotting a path back to international markets, which will be a vital element to not requiring further financing from its institutional creditors after next summer.

It is at that point that debt relief measures would kick in, gradually bringing with them lower fiscal targets and an easing of the pressure on Greece’s economy and its governments.

In soccer terms, the season is far from over, the manager has yet to prove himself and the goal is waiting for someone to put the ball in the back of the net.