Possible pressures on the public debt: Part 3

Greece deserves credit for improving the fiscal balance. To preserve this excellent progress, it is important to be alert to factors that can pressure the debt going forward – reality is always in flux. We have already mentioned two: fiscal operations that are not included in the reported fiscal balance, and the normalization of the effective interest rate on the debt. In this third Note on potential budgetary pressures, we consider how aging can impact the public finances.

Aging is found in the evolving demographic record and refers to the increase in the average age of the population. There are two main causes: Birth rates have slowed so there are fewer young people coming into the population, and medical knowledge is advancing and the standard of living is improving so people live longer.

Both forces cause the average age of the population to increase over time. The weights of different cohorts in the population are shifting toward elderly people and this has implications for the management of the public finances. Let us have a look.

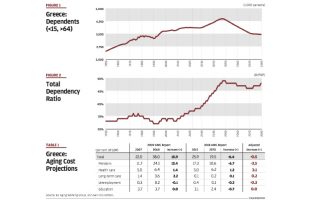

Figure 1 shows that the number of persons in Greece younger than 15 (school age) plus those over 64 (retirement age) is projected to increase from 2.5 million in 1950 to 4.5 million in 2050; thereafter this number is projected to ease to around 3.5 million by 2080. This is important because spending needs for young persons (education), and those of the elderly (retirement, healthcare, long-term care) will put pressure on the budget if there are more of them.

While the number of “dependents” is increasing, the total population is also increasing, so as long as there are more working-age people participating to produce output of goods and services, then the budgetary resources will also grow to help take care of dependents.

Figure 2 gives a sense how the dependent cohorts move in relation to the total population. It shows that the so-called total dependency ratio (dependents/population) was relatively stable through the turn of the century at around 35 percent, but that, looking forward, the dependency ratio will dramatically increase through 2050 before leveling off. The sharp increase in dependency from 2000-2050 is visible in many countries, and requires careful planning for future budgets.

The European Commission’s Aging Working Group (AWG) has been tracking the fiscal implications of aging since 2009, with follow-up reports every three years. This group of all member-states of the European Union makes projections, based on demographic factors alluded to, for fiscal spending needs given the legislation in place for social programs in each country, including Greece. The group specifically assesses incremental spending needs for pensions, long-term care, healthcare, education, and unemployment benefits over the horizon of some 50-60 years. Table 1 provides the results of these studies for “aging” costs for Greece in the 2009 report and the 2018 report.

The results for 2018 as compared with 2009 are truly remarkable. The AWG projects that during the crisis, in various rounds of pension cuts and changes to entitlement programs, Greece has lowered its cumulative aging costs by some 22.3 percentage points of gross domestic product (from +15.9 to -6.4). I have never seen a turnaround of this magnitude in any country. While the projections are likely to be revised somewhat in future as better and more precise information becomes available, it is nevertheless a further indication of the tremendous efforts made by Greece to deal with the crisis.

Also, a cut in future entitlement spending of this magnitude tends to affect the current population because it conveys pressure on them to help absorb the cost of their own days of aging. When people know that there will be less aging related transfers to them in the future, they become more cautious in their spending plans. Families sustained a large cut in their intertemporal wealth, and no wonder that growth fell precipitously during the crisis.

The loss to families in Greece from the intertemporal cut in their welfare expectations is a gain for the budget. Thus, on face value, this reduction in future costs, if the calculations are correct, will moderate future tax pressure and help debt sustainability, unless the political system were to convert these savings in entitlement spending into new spending. I am not sure that the debt sustainability analyses either in the EU or in the International Monetary Fund have taken explicit account of these effects.

There is a catch to these projections. The EU has nominal GDP growth assumptions (average around 3 percent a year) that are approximately 0.5 percentage point higher than my projections of future GDP nominal growth (average around 2.5 percent a year) in earlier Notes for Discussion. This lower nominal growth, compounded over 53 years (2017-2070) means that the level of GDP in the calculations in previous Notes for Discussion is some 30 percent less by 2070 than the level of GDP assumed in the long-run projections of the EU.

In turn, this means that the ratio of entitlement spending to GDP in the EU projections by 2070 needs to be adjusted for this lower denominator effect. When I do that, the ratio of future entitlement spending to GDP still drops, but by a smaller amount. The savings through 2070 are now projected to be 0.5 percentage point of GDP, as shown in the last column of Table 1.

Compared to calculations about fiscal sustainability that I made in 2009, the future for Greece looks more promising now and that is due to the policy efforts made during the crisis. Three effects may be mentioned: In 2009, the budget deficit was 15.4 percent of GDP and the aging costs were an increase of 15.9 percent of GDP (table above) that were projected on top of that deficit as a starting point. The new calculations depart from approximate balance in the budget in 2017 (a much better starting position) and the (adjusted) aging costs are a small reduction of 0.5 percent of GDP (table above).

The vast majority of the public may only see the improvement in the annual budget balance; they may miss the intertemporal improvement in the aging costs even though these are also real achievements in fiscal policy. The third factor that is relevant has a large negative impact on sustainability, namely the level of GDP that was used to make projections in 2009 was much higher than the projections for GDP that we are using now – this is the cost of the shrinking economy during the recession.

We will analyze in the next Note for Discussion how all the factors of demographics and for the public finances come together in a consistent long-run projection of fiscal sustainability.

Closing thoughts

The projections from the Commission’s Aging Working Group are carefully prepared and are the best we have. If these projections hold up in future, then Greece has eliminated its large incremental aging costs that had been projected in 2009, before the crisis began.

This is a policy achievement that has not received the recognition it deserves; perhaps because these calculations are tentative and less intuitive than looking at the reduction of the budget deficit year-by-year.

The large positive effect from eliminating aging costs has to be weighed against lower GDP that is now projected as compared to before the crisis. How these two factors, and others mentioned before, balance out for fiscal sustainability will be considered in the next Note for Discussion.

The projections of the Aging Working Group change every three years. They are influenced by GDP developments, demographic updates, and especially, fiscal policy. If the government undoes some of the social reforms, the aging costs will again go up in future (cancellation of the January 2019 pension cuts is not in the projections above; this would be a new setback).

Thus, it is crucial that the government has a small dedicated group of inter-agency experts to monitor the developments in aging costs for each budget round, and can calculate the proximate intertemporal impact of policy changes to the long-run sustainability of the public finances. Short-term noise should be ignored and policy should be oriented to the long run with a view on sustainability.

Clearly, the demands on government to carefully explain to the citizens what this is all about are high. Good communication and building trust is key.

One final thought. Even though it appears that the entitlement system, especially the pension system, has been recalibrated with parametric reforms to bring future costs in better balance with expected income, the underlying structure of the system itself, which is a so-called pay-as-you-go system run by the government, has not. This is important, because the microeconomic features of the current system remain suboptimal and can hurt competitiveness and incentives to strengthen saving and investment.

Thus, there is a large unaddressed agenda for pension system reform. Greek researchers are well aware of this problem and have made significant proposals to this effect, but the government has not engaged in a discussion on what to do.

* Bob Traa is an independent economist. This is the 12th in a series of articles by him for Kathimerini titled “Notes for Discussion – Essays on the Greek Macroeconomy.”