The Confessions of Saint Augustine

In August 2018, Greece exited the economic programs with the European partner countries, the European Commission, European Stability Mechanism, European Central Bank, and the International Monetary Fund (the latter had already opted out). This was seen as an occasion for celebration. Indeed, the economy is growing again, unemployment is coming down, the authorities report that they have been running fiscal surpluses since 2016, are committed to the privatization program, and have a growth strategy. Elections are in 2019. But the debt is still high, so arrangements were made with creditors to keep debt service manageable until the 2030s. So, there is some time to rev the engine of growth. If Greece reaches cruising speed before the 2030s, the challenges that are foreseen “in the long run” will be more manageable.

In his magnificent book from the year 401 “The Confessions of St Augustine,” St Augustine explains that he was a man from a small village in Roman Algeria who had an epiphany and turned to religion. The “Confessions” made him a pillar of Catholic doctrine. Before he was a saint, he was Not. And that was with a capital “N.” He lived a wanton life, boozed, gambled, lied, lived with loose women in sin, and broke just about every commandment in The Book. This life caught up with him and he collapsed physically and emotionally.

What made him so famous and useful for Catholic doctrine is the power of redemption. No matter what our sins have been, we can enter the Kingdom of Heaven if we repent and turn toward the Lord. It has to be a true conversion, said St Augustine, because the Lord knows everything.

This is where St Augustine really learned a few things. One is that you have to be serious. At first, when he had an inkling that not all was going well, he got on his knees, put his hands together, closed his eyes, and said:

“Oh Lord, give me chastity, but do not give it yet.”

He found out that this did not work. But then he repented in earnest and found redemption. And because he had fallen just as low as a man can fall, the Church thought that his resurrection was a miracle, a sign, and elevated this humble servant to sainthood. One can read his book from a philosophical or theological point of view – it is equally magnificent in both directions.

Greece is very desperate to lower the debt. The country has suffered enough. The political system has new plans to restart growth. All parties have their own plan. So, we all get down on our knees, put our hands together, close our eyes, and say:

“Please stand by so that we lower the debt, but not yet.”

The annual Article IV Consultation on Greece by the IMF for 2018 captures this sense exactly, but without once saying it out loud, and it may escape many readers:

– Growth has restarted and is projected to continue.

– Unemployment will gradually decline.

– The country is exiting the adjustment programs and the mood is improving.

– The government is running a reported surplus, which ought to be cash-flow positive.

– The government continues the privatization program, which is also cash-flow positive.

– The rating agencies are improving their ratings on Greece, even though the country is running arrears, and thus some obligations are in default and the debt is “in distress.”

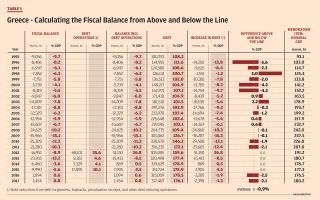

– But the capstone is: The debt in 2018 will increase by 21 billion euros (11 percent of GDP).

Wait a minute, how can this be? There is a fiscal surplus bringing in cash, privatization brings in more cash, but the debt is booming? This does not add up.

But some would say that it does add up, because new debt is meant to pay off 4 billion euros in arrears, and the government is building a big cash cushion in deposits. Let us consider this:

– If paying off arrears now results in an increase in the debt, then the arrears must not have been counted as debt before. I recommend against this. Arrears are obligations that are overdue and thus are debt. The legal definition and sundry niceties in accounting may not see this as legal debt, but the economics is crystal-clear: Arrears are debt. This debt is in distress. Do rating agencies ignore this?

– The government is building a big cash cushion and is apparently willing to borrow long-term debt to finance it. But if you run a surplus, then you are building a cash cushion, so why borrow and pay more interest? The 2018 surplus is projected at 1-2 billion euros. The privatization program is projected to bring in another 1-2 billion or so. If policy is cash-flow positive (and projected to remain so), and debt is sky-high and the debt is the key source of your grief, why borrow more?

The government says that it has “fiscal space.” What does this mean? In my view, fiscal space is a euphemism for “more spending to come” (or tax cuts, depending on what party you are from). Indeed, the government sees “fiscal space” of 0.4 percent of GDP in 2019, rising to 1.7 percent of GDP in 2022. Be assured, what space? These are huge amounts for a country that is drowning in debt. How do they do it? Well, by drawing on the cushion of deposits, of course. So, I interpret the cushion of deposits at the conclusion of the program as an advance, a reserve, to boost spending. This is St Augustine before he had the real epiphany:

“Please give me strength to lower my debt, but not yet.”

Did Odysseus and his fleet make a false start? I sincerely hope that there will not be more tears for the average Greek family.

Bob Traa is an independent economist. This is the 14th in a series of articles by him for Kathimerini titled “Notes for Discussion – Essays on the Greek Macroeconomy.”