Solvency depends on Greece’s willingness to continue with fiscal recovery

As presented in the previous Note for Discussion, the intertemporal balance sheet calculated as of 2009 (version 2009) – and its projections – was preliminary and data and economic policies have since been revised.

The crisis has led several Greek governments since then to take many measures to address the dire state of the public finances. Thus, we can now ask whether all this effort has improved the balance sheet as of year-end data for 2017 (the version calculated in 2018), now that we are nine years on and the country is emerging from the recession.

There are some important differences in the starting position in 2018 as compared with 2009. On the upside, the fiscal balance is in much better shape, and many (difficult) measures were taken to reduce unfunded promises in the social welfare state and bring future aging costs down.

On the downside, the debt ratio is higher today, and the outlook for future GDP is subdued due to revisions in the demographic projections. It is the balance of all these factors, and especially the willingness of the Greek political system to stay the course of stronger fiscal policies into the future (as suggested by Odysseus’ Plan in Note for Discussion 13), that determines whether the intertemporal balance sheet has achieved solvency. Let us have a look.

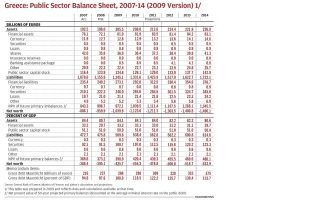

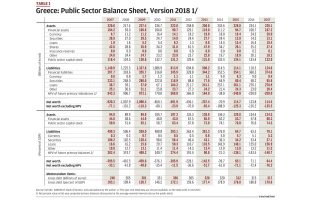

Table 1 updates the results from the 2009 version to the 2018 version. Key updates are as follows:

Financial assets and financial liabilities were updated with the published results through end-2017 by the Bank of Greece. The new statistics show that holdings of financial assets as well as liabilities were increased for the past, suggesting more precise measurement and a better definition of the fiscal perimeter. Over time, the amount of financial assets owned by the public sector has remained in a narrow band of around 106 billion euros. Liabilities have increased, however, from around 300 billion euros at end-2007 to some 375 billion at end-2017 (mainly reflecting increased debt during the crisis years).

I have updated the estimates for the public sector capital stock with the same method (the “perpetual inventory method,” or PIM) that was used for the balance sheet version of 2009. This reveals that the estimated net depreciated capital stock is staying relatively stable at around 130 billion euros, or some 74 percent of GDP (the capital stock in euros has remained fairly stable, but GDP has dropped).

If we combine assets with financial liabilities to proxy a “traditional balance sheet” then we find that net worth of the Greek public sector, based on these data, is slowly worsening over time, from -33 percent of GDP at end-2007 to -76 percent of GDP at end-2017. This is not a good number, but the decline in GDP during the crisis must be considered, and with better overall fiscal balance and a restarting of growth, there ought to be room for some recovery in this number as the country moves forward.

The biggest improvement in the update comes from the dynamic forward-looking part of the intertemporal balance sheet. The net present value (NPV) of future primary balances now reflects a time horizon of 60 years (it was 50 years in the 2009 edition). The projections assume that Greece stays the course of Odysseus’ Plan of fiscal recovery to a debt ratio of 60 percent of GDP or below, which would be achieved by around 2080 as explained in Note for Discussion 13. This is crucial – if the political system does not like this plan and alters the objectives for fiscal policy, then the NPV of future costs under the welfare state will change and the balance sheet will change as well – which would then need to be recalculated in a future iteration.**

If Greece can stick to the plan as sketched over time, the intertemporal net worth of the public sector as of end-2017 is now positive at +64 percent of GDP. The data between 2009 and 2015, for which I do not have independent annual calculations of the NPV, are interpolated. For 2015, 2016 and 2017, I have calculated the 60-year implications of “policies in place.”

Table 1 is remarkable. In the update of version 2018, and because of the many difficult measures implemented since 2009, the significant progress in eliminating the fiscal deficit, the assistance of partner countries to lower the interest bill for the government, the record-breaking haircut on Greek debt by the private sector in 2012 (the PSI), and despite shifting down the GDP outlook for decades to come based on weaker demographics, at end-2017 Greece’s intertemporal net worth appeared slightly positive and relatively stable, instead of deeply negative and deteriorating as in the version of 2009.

This indicates that the long-run Odysseus Plan to bring the debt down by 2080 would make the Greek fiscal system solvent again. It does not guarantee that the Greek political system will stick to this path (as indicated, some policy reversals have already been implemented). But an improved perspective of solvency has opened up, and that did not exist before. Greece and partner countries deserve much credit for the difficult steps that have been taken to come to this improved starting-off point.

That Greece has a chance at long-run solvency may come as a surprise to some readers. There has been huge stress for the Greek population while the adjustment programs were being implemented. The reason that these programs are so difficult politically, is that the public cannot see why the difficult measures are necessary to restore solvency – they only see short-term austerity – this is a communications issue. Without an intertemporal balance sheet and a continued dynamic thermometer of the public sector net worth, improvements for the future have little real value for the public.

But in the economics profession, the value (NPV) of these long-run plans and efforts can be calculated and reflected in the intertemporal balance sheet to show progress, as I have attempted to demonstrate in these Notes for Discussion. That is why governments should start to show the intertemporal balance sheet in their annual budget documents, and duly update this reporting once a year with new data and projections under policies then in place.

The methodology that we have used to sketch the path home is not excessively difficult and the task I recommend is doable. If the government shows the long-run consequences of its policy decisions together with the budget document, then budgetary policy gets tightly integrated with a view of long-run sustainability of the public finances, and that is a valuable aspect to know for voters.

Also, interested observers can then check whether the government is on track to deliver a desired path. There may be other paths that are better, or more feasible from a socioeconomic and political point of view, but they will have a chance to discuss this alternative path and see if it could be implemented and deliver intertemporal solvency as well. This would vastly enrich the discussion on public financial policies.

As we have said before, there will be ups and downs, and there will be shocks, some positive, others negative, that will confront the recovery to fiscal sustainability. But that is OK, it happens in all countries. If Greece is willing to operate with a strong conviction that solving the debt problem over a long-term horizon and restoring solvency is a worthy objective, and if the European partner countries can assist Greece along this path, then understandings can be reached to monitor progress and see how frequently important comprehensive calculations need to be updated and how to interpret and discuss alternative assumptions and assessments of risk along the way.

That will foster good policy-making and sound cooperation among partner countries.

The balance sheet of version 2018 is predicated on Greece staying the course of Odysseus’ Plan to get the country safely home. Since this is a demanding path, no matter how we look at it, it would be good if we could find opportunistic policies to get the debt down somewhat faster without the requirement to bolster the primary surplus further. In the next Note for Discussion, I will present one idea for such an opportunistic policy.

Bob Traa is an independent economist. This is the 23rd in a series of articles by him for Kathimerini titled “Notes for Discussion – Essays on the Greek Macroeconomy.”

Since these calculations were carried out, the government has further increased the national debt, increased minimum wages, and there are important changes under way to undo some of the savings in the pension system (all contrary to Odysseus’ Plan). Indeed, it looks as though some of the policies achieved under the previous adjustment programs have stopped or are being reversed. These effects, which worsen the long-run fiscal outlook, have not yet been calculated in this version 2018 of the balance sheet.