New inflation developments are rattling markets and economists. Here’s why.

When inflation began to accelerate in 2021, price pressures were clearly tied to the pandemic: Companies couldn’t produce cars, couches and computer games fast enough to keep up with demand from homebound consumers amid supply chain disruptions.

This year, Russia’s war in Ukraine sent fuel and food prices rocketing, exacerbating price pressures.

But now, as those sources of inflation show early signs of fading, the question is how much overall price increases will abate. And the answer is likely to be driven in part by what happens in one crucial area: the labor market.

Federal Reserve officials are laser-focused on job gains and wage growth as they quickly raise interest rates to constrain the economy and slow rapid price increases. Officials are convinced that they must sap the economy of some of its momentum to wrestle the worst inflation in four decades back down to their goal of 2%.

The way they do that is by slowing spending, hiring and wage gains — and they do that by raising the costs of borrowing. So far, a pronounced cool-down is proving elusive, suggesting to economists and investors that the central bank may need to be even more aggressive in its efforts to temper growth and bring inflation back down.

As data this week showed, prices continue to soar. And, while the job market has moderated somewhat, employers are still hiring at a solid clip and raising wages at the fastest pace in decades. That continued progress seems to be allowing consumers to keep spending, and it may give employers both the power and the motivation to increase their prices to cover their climbing labor costs.

As data this week showed, prices continue to soar. And, while the job market has moderated somewhat, employers are still hiring at a solid clip and raising wages at the fastest pace in decades. That continued progress seems to be allowing consumers to keep spending, and it may give employers both the power and the motivation to increase their prices to cover their climbing labor costs.

As inflationary forces chug along, economists said, the risk is rising that the Fed will clamp down on the economy so hard that America will be in for a rough landing — potentially one in which growth slumps and unemployment shoots higher.

It is becoming more likely “that it won’t be possible to wring inflation out of this economy without a proper recession and higher unemployment,” said Krishna Guha, who heads the global policy and central bank strategy team at Evercore ISI and who has been forecasting that the Fed can cool inflation without causing an outright recession.

The challenge for the Fed is that, more and more, price increases appear to be driven by long-lasting factors tied to the underlying economy, and less by one-off factors caused by the pandemic or the war in Ukraine.

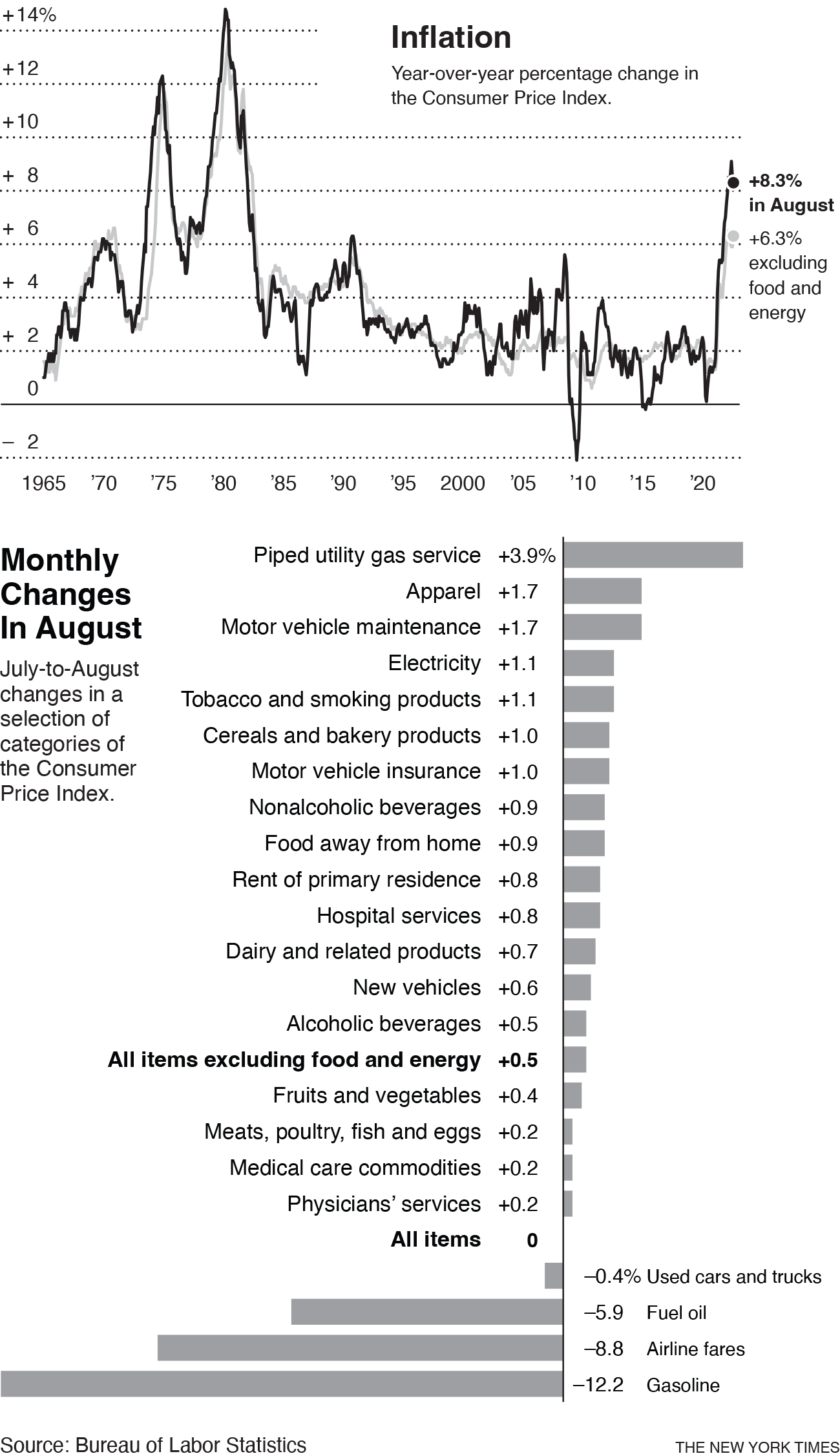

Consumer price index data from August released Tuesday illustrated that point. Gas prices dropped sharply last month, which many economists expected would pull overall inflation down. They also thought that recent improvements in the supply chain would moderate price increases for goods. Used car costs, a major contributor to inflation last year, are now declining.

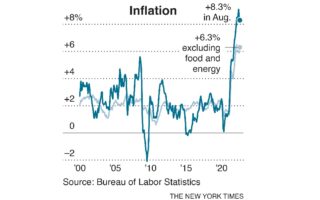

Yet, in spite of those positive developments, quickly rising costs across a wide array of products and services helped to push prices higher on a monthly basis. Rent, furniture, meals at restaurants and visits to the dentist are all growing more expensive. Inflation climbed 8.3% on an annual basis, and picked up by 0.1% from the prior month.

The data underscored that, even without extraordinary disruptions, so many products and services are now increasing in price that costs might continue ratcheting up. Core inflation, which strips out food and fuel costs to give a sense of underlying price trends, reaccelerated to 6.3% in August after easing to 5.9% in July.

“Inflation currently has a very large underlying component that is grounded in a red-hot labor market,” said Jason Furman, an economist at Harvard University. “And then, in any given month, you may get more inflation because of bad luck, like gas going up, or less because of good luck, like gas going down.”

He estimated that core inflation would continue to climb at around 4.5%, and rising, even if pandemic- and war-related disruptions stopped pushing prices higher.

For now, inflation provoked by war and supply chain disruptions isn’t entirely behind the United States — fighting in Ukraine continues and a railroad strike that threatened to roil critical American transit lines was narrowly avoided Thursday with a tentative deal. But there are hopeful signs that both are beginning to dissipate. Supply chains have started to unsnarl, and commodity prices for oil and some grains have dipped after surging amid Russia’s invasion of Ukraine.

That could pave the way for consistently slower consumer price increases, shifting the focus to how much, and how quickly, inflation can fall. The answers to those questions will hinge more on fundamentals.

“The bigger question for the Fed is not: Has inflation peaked? It’s: What’s the destination?” said Aneta Markowska, the chief financial economist at Jefferies. She estimates that it will be hard to get inflation below 4% — twice the Fed’s average goal of 2% — without a substantial slowdown in the economy and labor market.

“You still have housing and the labor market, and there’s still a lot of inflationary pressure radiating from those two areas, which are very unbalanced,” Markowska said.

That is why the Fed, which meets next week, is scrambling to bring supply and demand back into balance.

Central bankers have raised interest rates from near zero in March to a range of 2.25% to 2.5% at their last meeting, and are widely expected to lift them by at least another three-quarters of a percentage point next week. The Fed’s moves constitute its fastest campaign of rate increases since the 1980s. The goal is to make it expensive to borrow money, which in theory will cool consumer spending, allowing supply to catch up and prompting businesses to charge less as they compete for customers.

In the wake of Tuesday’s worrying inflation data, investors began to speculate that officials might make an even more drastic full-point rate increase next week, or that they might push rates higher than they otherwise would have in an effort to clamp down on the economy.

Economic growth, while slowing, has proved fairly resistant to the Fed’s rate changes so far. Consumption has tapered off, but it is not tanking. Employers hired 315,000 people last month, and a variety of wage measures show that pay is still climbing at an unusually rapid clip, albeit not enough to keep up with inflation.

The combination of more jobs and better pay is likely helping to shore up household finances, which were already bolstered by pandemic savings, giving families the ability to keep spending and the wherewithal to keep up with higher housing costs. At the same time, rising labor bills may be prompting some firms to raise prices to protect their profit margins.

“Inflation looks stickier and broader-based,” Allison Boxer, an economist at PIMCO, said following Tuesday’s report. “There are reasons to worry that we are shifting to wages being a bigger issue.”

Even before this week’s inflation data, Fed officials had suggested that they were not ready to slow their rapid pace of rate increases despite the glimmers of falling used car prices, calmer gas costs and more contained consumer inflation expectations.

“It is very much our view, and my view, that we need to act now, forthrightly, strongly, as we have been doing,” Fed Chair Jerome Powell said in remarks last week. “We need to keep at it until the job is done.”

It could be that the economy’s nascent slowdown is just taking time to feed through to company pricing behavior, and that underlying inflation will begin to fade, as officials have been hoping.

But if the Fed decides that it needs to constrain the economy more intensely in the coming months to achieve its goals, as investors are increasingly speculating, that could come at a cost.

Central bankers have been hoping to slow the economy enough to decrease job openings without harming it so much that unemployment jumps. Some economists still think that is possible, given how unusual labor market conditions are right now.

Yet, a faster, more drastic series of rate increases would heighten the chance of a sharp pullback in growth that pushes up unemployment.

America will get a glimpse of the Fed’s assessment of what is needed next week, when central bankers release both a rate decision and a fresh set of economic projections.

In their economic estimates in June, officials anticipated that interest rates would climb to a peak of 3.8% next year and that unemployment would rise only slightly from its current level of 3.7%. Economists increasingly project that both forecasts — interest rates and unemployment — could jump higher.

“The most plausible scenario is that inflation won’t come down unless unemployment goes up,” Furman said. “It is possible that the labor market could cool down without additional unemployment — it’s just never happened that way before.”

This article originally appeared in The New York Times.