FDI and the ‘export or die’ mentality: Will Greece make the leap forward?

During the past few weeks, the public discourse in Greece has been almost exclusively dominated by identity issues, arguments hailing from the distant past, and priorities which, however interesting and indeed very influential, are not significant enough to define the lines along which the real Greek drama could potentially develop. Growth and investments, however, are.

Despite the improvements, Greece’s economy has not yet been able to overcome the deep deterioration which it experienced over the past decade; and despite the flood of triumphal statements and proclamations made each and every day by the present Greek government, there is still not enough evidence to demonstrate that Greece has returned to a state of normalcy.

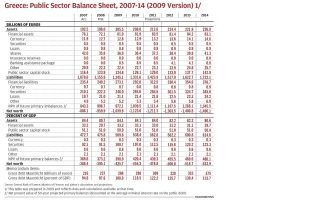

In fact, owing to the fact that it still has the highest public debt-to-gross domestic product ratio in the European Union, while also experiencing low inflation and sluggish public revenue, and the possibility of receiving further debt relief being especially unlikely, Greece’s potential to generate and sustain long-term growth is under question.

According to the 2018 Global Competitiveness Report carried out by the World Economic Forum, Greece ranked in 57th place among 140 countries in the area of national economic competitiveness, with fellow Southeast European countries such as Bulgaria and Romania performing substantially better.

Another important area where Greece systematically underperforms is in attracting investments. A recent PricewaterhouseCoopers survey concluded that the amount of investment needed to add three to four percentage points to the country’s GDP amounts to about 210 billion euros for the period from 2018 to 2022. And despite the fact that Greece is expected to secure almost 100 billion euros in the same period, there is still a funding gap of about 110 billion euros to be filled.

Alas, this investment gap of 10-12 percent of GDP can be filled neither by public investments – given the fiscal limitations of the Greek public sector – nor by private domestic capital, which is constrained by limited bank lending and generally tight credit conditions in the country as well as low corporate profits and declining savings.

Hence, what is becoming pretty obvious is that Greece’s road to real growth is closely linked to its ability to attract foreign direct investments.

Indeed Greece’s structurally discouraging business environment and problematic institutional framework does not facilitate foreign direct investment inflows, which in 2017 reached only 1.78 percent of gross domestic product, according to the World Bank (a score significantly lower than countries such as Spain and Portugal).

High taxes, the overregulation of markets and professions, enhanced corruption and a cumbersome judicial and administrative system are just some of the many barriers to foreign investors. So for Greece to make the great leap forward, it should carry out numerous policy reforms including the deregulation of the economy, a reduction of taxes and social security costs, the minimization of administrative impediments and the improvement of the judicial system.

What is, however, of equal importance is to identify the industries that may have better export potential than the goods and services Greece exports today and design policies aimed at attracting foreign direct investment in those specific sectors.

What differentiates a recent study published by IHS Markit, titled “How Can Greece’s Economy Achieve Sustainable Growth,” is that the authors, paradoxically enough, suggest that Greece should focus on attracting FDI in sectors such as aircraft and spacecraft manufacturing, shipbuilding, and machinery and equipment production, rather than pouring more money into traditional industries such as tourism and agriculture.

The study concludes that a concentration of future investment in tourism, agriculture and the food industry will only result in short-term economic benefits, generating constant unbalanced growth and perpetuating Greece’s reliance on imports.

On the other hand, prioritizing foreign direct investment in the three abovementioned “heavy” industrial sectors – aircraft and spacecraft manufacturing, shipbuilding, and machinery and equipment production – will trigger a “virtuous cycle,” as other industries will start investing to supply the industries benefiting from the original FDI inflow, hence reducing unemployment, boosting exports, creating additional income and then gradually relieving credit constraints for businesses and households.

The IHS Markit study further indicates that in order to boost an investment recovery, a concrete package of bold reforms should be designed and implemented, comprising such features as elimination of employer and employee social security contributions, an end to pensions for people under 67 and the introduction of a flat pension schedule for people over that age, the maintenance of a stable fiscal environment and the implementation of reforms aimed specifically at boosting foreign direct investment in export-oriented industries.

IHS Markit assumes that a high, albeit reachable, level of FDI inflow in the given sectors could raise Greece’s gross domestic product by 2.5 percent in 2020 and by 7.4 percent in 2024.

However, what is necessary to proceed to such a paradigm shift and such revolutionary reforms is bold, innovative and future-oriented political leadership that is determined to adopt an extrovert “export or die” mentality – exactly what Greece lacks right now.

* Vassilis Gavalas is a political analyst cooperating with the think tank DIKTYO – Network for Reform in Greece and Europe.