Inflation should be kept below but near 2 pct a year

In the previous Notes for Discussion we considered population and demographics as one fundamental anchor for the size of the macroeconomy and how fast an economy is able to grow in the future. We also introduced productivity per person employed as the fundamental anchor for the level of per capita income in the economy. In the end, only productivity improvements can lift the economic standard of living of the population, on average.

The interaction between demographic developments and labor productivity determines the amount of goods and services that an economy can produce, known as real GDP. It is now time to combine this analysis with a consideration of average prices for these goods and services. This provides a view on nominal GDP and inflation, as defined by the implicit GDP deflator (1).

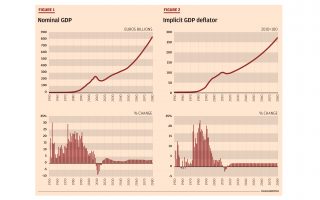

Figure 1 shows the path of nominal GDP since 1950, and my baseline projection scenario for nominal GDP from 2018 through 2080. This projection scenario takes as a starting point the growth in real GDP that we had derived from demographic developments and an aspirational assumption about the growth in labor productivity, combined with the expectation that, going forward, the average price level of GDP – the implicit GDP deflator – will grow by 1.75 percent a year.

It remains important to acknowledge that the future will not be linear and smooth, as is depicted in this scenario, but rather will be volatile over time. What this scenario is designed to do is proxy the “average” or “realistic” or “most likely” scenario, in my view, given the assumptions that are clearly stated. The government and other analysts may have different scenarios, and, if so, it would be good to discuss these with the public, so that voters are always well informed about different views and options.

The great benefit of having such a scenario, for policy makers and the public alike, is that it provides a benchmark that can be monitored over time to see if policies provide the desired results. I show annual numbers, but the underlying quarterly numbers can be extracted from this scenario (as will be shown later) so that everyone can evaluate on a quarter-by-quarter basis whether the economy is behaving as expected and, if not, why results may be better or worse than we had thought. Without overreacting to quarterly ups and downs, policy making rooted in a quantified scenario tends to impart accountability and the need for dialogue that might otherwise be missing. Good communication with the public supports confidence, even if reality is difficult to predict.

What are some of the interesting features of the Greek economy over this long interval? We see the decline in nominal GDP over 2009-2016. This is highly unusual as nominal economies almost never decline, and it is an indication of the severity of the recession. A local maximum was reached in 2008, when GDP reached 242 billion euros – this declined to a local minimum of 174 billion euros in 2016. It represents a loss of 28 percent of nominal GDP. Fortunately, nominal GDP is now growing again and the scenario projects it to continue growing at subdued rates of 2.5 percent average in the future, as shown in the lower panel of this picture. The figure indicates that a mild rebound may be expected in the 2020s, followed by lower nominal growth in the 2030-2040s, before settling at growth of around 2.5-2.75 percent a year in the long run, given the assumptions that we have made. At an intuitive level, we can think of real growth of around 0.74 percent, and inflation, as per the GDP deflator, of 1.75 percent in the very long run.

This subdued nominal growth outlook is important for policy making: Fiscal policy is grafted upon nominal variables and nominal GDP. We often try to see the path for fiscal variables in relation to nominal GDP – the scalar for most fiscal analysis. When an economy is growing moderately in the future, then the pace of fiscal expansion also must be moderate, lest the country risk running into big deficits again and rebuild debt. Indeed, it is easier to deal with debt problems when nominal GDP grows fast, as compared when nominal GDP growth is moderate. Thus, expectations about fiscal stimulus to jump-start the economy in future must be scaled down appropriately.

The limits for fiscal policy were less stringent in the past when Greek nominal GDP grew by as much as 20 percent a year (1970s-1980s in the picture above); but this growth was mostly due to inflation, not real growth. Inflation is a tax on the cash economy and yields an advantage for the Treasury, which contributes to controlling the deficit and the debt. But Greece is now in the eurozone and inflation in the eurozone is “at or below 2 percent a year” as targeted by the European Central Bank. Moderate inflation has many benefits, especially for the poor, as compared to inflation of 20 percent, but it does put an extra demand on the fiscal authorities and political system, who need to run the budget with great discipline.

Figure 2 shows the GDP deflator, which is the result of deflating nominal GDP with real GDP growth (hence it is called the “implicit” GDP deflator). It is obvious that the 1970s-1980s were high inflation times for Greece. Then Greece started to prepare for entry into the eurozone and brought inflation down to around 2 percent at euro entry, followed by a period in the high growth years of the 2000s of inflation around 3 percent. The latter is too high for an economy that is attached to an anchor designed for 2 percent or below. This huge anchor can drag the ship down as the water level inflates by 3 percent on average – domestic Greek inflation around 1 percent a year higher than in the eurozone on average. This is precisely what happened and why Greece lost competitiveness in the 2000s. The reckoning from this overshooting, or overheating, came in the form of the deep recession.

If Greece is to thrive in the eurozone, then the GDP deflator should evolve according to “below but close to 2 percent a year.” We have pitched our assumption for the future GDP deflator at 1.75 percent to present a scenario where the policy intentions are consistent with the stated preferences for eurozone inflation. If Greece does not share this policy objective of the ECB, then success for Greece will likely prove fleeting. For our scenario, we have assumed a consistent stance of domestic policy in the long run with ECB policy.

Closing thoughts

* A comprehensive picture is starting to emerge for the Greek macroeconomy. We have looked at demographics to determine the size of the economy, and labor productivity as the final source for the economic standard of living.

We have now complemented these “real economy” real GDP variables with a constraint on how fast prices can grow in the economy in the long run, to derive a scenario for the proximate size of the nominal economy – nominal GDP.

* Now that we have the building blocks of demographics, productivity and inflation, we can start analyzing how economic policy making is related to these variables and what degrees of freedom such policy making enjoys. If policy makers ignore or deny the fundamental building blocks of the economy, then something is going to go wrong somewhere in the economy and that will depress growth and the standard of living over the long run.

* Having a quantified scenario for the economy will help to monitor developments as they occur, and it will also provide possible clues that may require an adjustment in the scenario – nature will reveal gradually over time whether the economy is on track to deliver the sketched scenario or not. Close monitoring, good communication, and being prepared to make some adaptations to policy is the key to building confidence and stabilizing growth going forward.

* We have derived a “price vector” above, the path for the GDP deflator. One question that now emerges is whether this price vector is consistent with restoring external competitiveness for the economy and how this process is to be done (for success in any general equilibrium system where everything is attached to everything, all variables have to be in balance). We can turn to that question in the next Note for Discussion.

Bob Traa is an independent economist. This is the seventh in a series of articles by him for Kathimerini titled “Notes for Discussion – Essays on the Greek Macroeconomy.”

(1) Thus, nominal GDP equals the amount of goods and services produced times the current prices that are charged for these goods and services. Nominal GDP can change because the amount of goods and services can increase or decrease (that is real GDP) and/or because the prices for these goods and services can change (inflation or deflation). Average prices, as measured from nominal and real GDP, are called the implicit GDP price deflator.