After vote on measures, which way next?

Between the government’s claims that the volume of expansionary countermeasures it agreed with Greece’s lenders outstrips the fiscal interventions it will have to make in the coming years, and the opposition’s mantra that Prime Minister Alexis Tsipras has agreed a fourth memorandum of understanding without any funding, it was difficult for MPs and voters to know whether they were coming or going ahead of last Thursday’s multi-bill vote.

The measures may have been passed last week, consigning them to parliamentary history, but their impact will be felt in the coming years. Therefore, it is worth delving a little deeper into the content of the omnibus bill and weighing up what it may mean for Greece going forward.

In this respect, perhaps the last pages of the 245-page multi-bill were the most important as they contained the Medium-Term Fiscal Strategy (MTFS) for 2018-21, which sets out the crucial macroeconomic and fiscal forecasts and targets for the coming years.

On the macro side, the numbers are not the most encouraging. The projection for growth this year has been reduced from 2.7 percent of gross domestic product (which few thought achievable even under the best of circumstances) to the more realistic 1.8 percent, which is below what the European Commission and the International Monetary Fund have predicted.

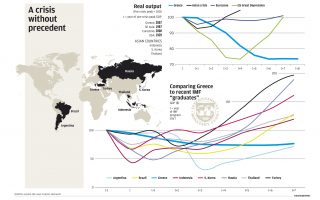

The immediate question that arises is whether this fairly modest goal is achievable. The GDP data for the first quarter of 2017 published last week suggest that it is not going to be a straightforward proposition. The flash estimate from the Hellenic Statistical Authority (ELSTAT) showed that GDP contracted by 0.1 percent quarter-on-quarter (or 0.5 percent year-on-year) in Q1. Although this was a smaller shrinkage than many expected due to the protracted negotiations over the second review, it officially tipped Greece back into recession after a short-lived period of small growth in 2016.

What makes this slip even more vexing is that GDP in the eurozone was up by 0.5 percent in the first quarter of the year. Greece was the only member of the euro area to report a negative figure. Portugal saw its strongest growth for a decade in Q1, rubbing more salt into Greek wounds.

One could try to look at the positive and argue that the strengthening of the eurozone economy may help create a more beneficial environment in which Greece can grow. After all, they say a rising tide lifts all boats. However, the prevailing economic environment in the eurozone is just one of the factors that will determine Greece’s immediate future.

The forecasts contained in the MTFS do not suggest that Greeks should expect soaring growth in the next few years. GDP is seen rising by another 2.4 percent in 2018, 2.6 percent in 2019 and then easing to 2.3 percent in 2020 and 2.2 percent in 2021. To put this into perspective, Ireland, one of the eurozone’s former adjustment program countries, saw its economy expand by 5.2 percent last year.

It is no surprise, though, that Greece can only dream of such numbers. Apart from having to overcome the toll of almost a decade of near-continuous recession, Greece will continue to put pressure on its economy in the coming years through more austerity measures.

The policies included in the multi-bill will see measures worth 2.63 billion euros adopted in 2019 and another 1.92 billion in 2020, on top of around 500 million euros of measures that are lined up for next year to close the fiscal gap.

In Greece’s position, after seven years of non-stop fiscal adjustment, this is a considerable economic burden to bear. The government argues that the countermeasures it will implement if it meets its fiscal targets can balance out the impact of the pension cuts and the reduction to the tax-free threshold for personal incomes.

The expansionary interventions that Athens can implement in 2019 are on the spending side and will reach a maximum of 2.65 billion euros. The following year, should everything go according to plan, the government will be able to provide another 1.92 billion euros in tax relief.

During this period, Greece will still be producing a primary surplus of around 8 billion euros or more, equivalent 3.5 to 4 percent of GDP. After years of deficits, Greece produced a primary surplus of about 0.8 percent of GDP in 2013 and has been building on this ever since. Athens will likely be required to produce large primary surpluses for at least another five years.

A few years ago, economists Barry Eichengreen and Ugo Panizza studied a sample of 54 emerging and advanced economies between 1974-2013 to see what type of economic and political variables are associated with large and persistent primary surpluses. In 15 percent of cases surveyed there were primary surpluses of at least 3 percent of GDP for at least five years. “Larger and longer primary surplus episodes are rarer. Primary surpluses as large as 4 percent of GDP that last for at least a decade are extremely rare,” the economists found.

Combining such a high budget surplus with ambitions for strong growth does not make the greatest economic sense. It is instead, a reflection of the contrary situation in which Greece and its lenders have got themselves into, digging a deeper hole that becomes ever harder to get out of.

A prime illustration is that Greece will have to implement the fiscal measures lined up for 2020 a year earlier if it is not on track to meet its primary surplus target. Yet, the most likely reason for Greece falling short would be its economy not growing enough to generate the public revenues needed for the surplus. The most probable cause for the economy underperforming would be the constrictive impact of the efforts to meet high fiscal targets. Yet, the response to this would be to pile all the measures on in 2019.

It will, therefore, be a blessing for everyone if the best possible scenario plays out over the coming years. Greece’s lenders have a chance to influence events when they gather for Monday’s Eurogroup to discuss medium-term debt relief measures and the fiscal path for the coming years.

If they are able to reach an agreement on what steps to take from next summer to gradually bring Greece’s public debt down to sustainable levels, this will also allow them to lower the fiscal targets Athens has to achieve in the near future. Both are vital for Greece’s prospects.

The numbers scattered throughout the multi-bill that coalition deputies approved on Thursday all point to the same thing: Greece cannot convincingly grow its way out of the crisis in the next years unless it receives significant assistance. Only then will we know what direction we are heading in.